Anyone who earns a monthly or weekly salary, and has a household to run, must consider all the regular bills that must be paid and all other expenses that must be met, even before they harbour any thought of saving or money for optional expenses, like entertainment.

The government is no different. Revenues from taxes, administrative services and other sources sum up the total earnings of the state; and strict accounting measures must be applied to determine the best money measures to pursue.

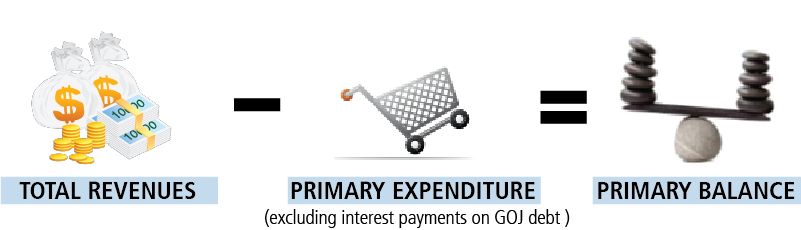

Fiscal accounts can be defined as what is left to service debt, after the government pits its revenue against its expenditure.

So, wages, social programmes spending, and general spending on maintaining the country, is taken out of revenues, and what is left is called the primary surplus.

Governments always have pre-set primary surplus targets and very few have managed to meet them. Under the current IMF agreement, the target for Jamaica’s primary surplus is 7 per cent of Gross Domestic Product (GDP). At the moment, Jamaica is set to meet this target at the next IMF review.

As explained by EPOC co-chair, Keith Duncan, there are several reforms that Jamaica must undertake, under the current arrangement. These changes include adjustments to the public sector wage bill, the system governing taxes and other critical monetary factors, all of which will push us towards our goal and meet the agreed primary surplus target.

“Our job at the EPOC continues to be to support the process of maintaining public awareness and to play an effective monitoring role. EPOC will continue to hold our Government accountable for this new economic programme, primarily as it relates to the fiscal and monetary policy commitments that we have made.”

EPOC is closely monitoring this target, as it is key to the overall performance of the nation, under the current programme.

{kind=link}